Buying Life Insurance For Parents: What Steps (You) Need To Know

Free Life Insurance Comparison

Compare Quotes From Top Companies and Save

Leslie Kasperowicz

Farmers CSR for 4 Years

Leslie Kasperowicz holds a BA in Social Sciences from the University of Winnipeg. She spent several years as a Farmers Insurance CSR, gaining a solid understanding of insurance products including home, life, auto, and commercial and working directly with insurance customers to understand their needs. She has since used that knowledge in her more than ten years as a writer, largely in the insur...

Farmers CSR for 4 Years

UPDATED: Dec 4, 2023

It’s all about you. We want to help you make the right life insurance coverage choices.

Advertiser Disclosure: We strive to help you make confident life insurance decisions. Comparison shopping should be easy. We are not affiliated with any one life insurance provider and cannot guarantee quotes from any single provider.

Our insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different life insurance companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about life insurance. Our goal is to be an objective, third-party resource for everything life insurance-related. We update our site regularly, and all content is reviewed by life insurance experts.

UPDATED: Dec 4, 2023

It’s all about you. We want to help you make the right life insurance coverage choices.

Advertiser Disclosure: We strive to help you make confident life insurance decisions. Comparison shopping should be easy. We are not affiliated with any one life insurance provider and cannot guarantee quotes from any single provider.

Our insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different life insurance companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

On This Page

Quick Tip

As the child of an elderly parent, you may be wondering if it’s possible to purchase a life insurance policy on them? The quick and short answer is yes, you can! It’s not uncommon at all for adult children to purchase, make payments and even own a life insurance policy on mom and dad.

Although about 90% of people agree that life insurance is important, only about 60% of people have it.

Whether it’s because people don’t like talking about death or because they feel it’s too complicated, too many families don’t talk about life insurance until it’s too late. If you’re avoiding the conversation, it might be time to tackle the issue head-on and start talking about life insurance for parents.

While you want your parents to live long happy lives, to see grandkids grow up and enjoy the things they love, death is a fact of life. And it’s that same matter-of-fact attitude that you and your family should take when talking about life insurance.

It’s a hard conversation to have when someone is sick and emotions are high.

Everyone is better off taking care of buying life insurance for parents while everyone is healthy and in good spirits. If you’re ready to start looking into this, here are the things you need to know.

Looking to compare life insurance prices? We can help. Enter your ZIP code to get free quotes from multiple insurers.

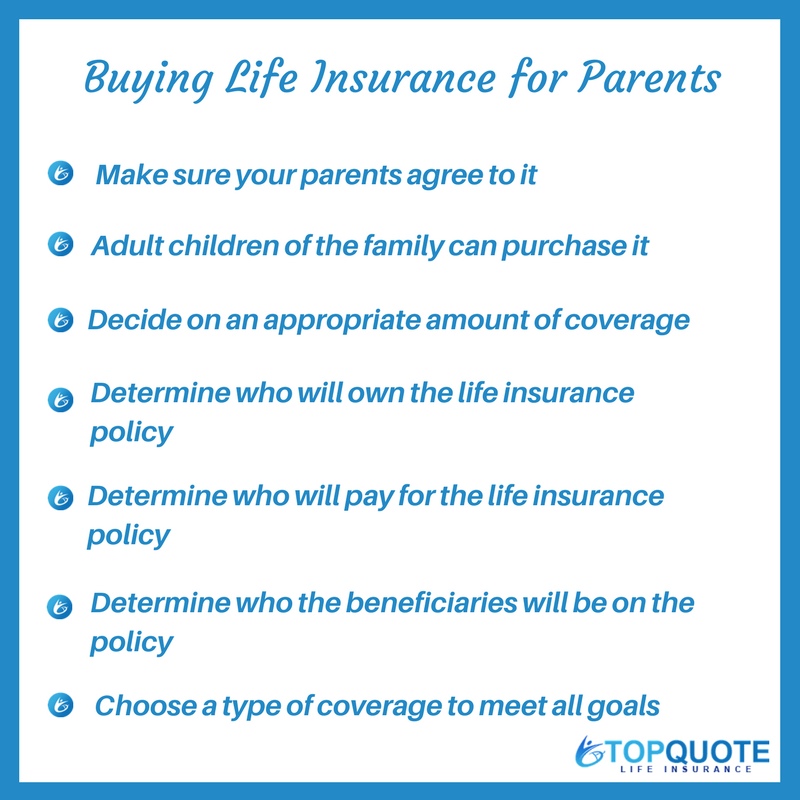

Quick Tips for Buying a Life Insurance Policy on your Parents

#1. Consent Is Key When Looking Into Life Insurance For Parents

Before you purchase life insurance for parents, you need to make sure you have their written agreement.

This is true for anyone you might buy life insurance for. The written consent allows life insurance companies to avoid giving out policies to anyone who might have ill intentions on someone else.

It’s kind of a dark thought, but “foul play” incidents that aim to get someone’s life insurance to have a long history. Your relationship with your parents isn’t a question. This just protects the insurance company.

Companies and legal professionals agree that it’s unethical to take out a life insurance policy on anyone without their knowledge.

IMPORTANT:

Written consent will often come in the form of your parent signing as the insured on the life insurance application. Your parents signature on the application provides proof to the insurance company that your parent is aware of a potential life insurance policy being taken out on them.

Depending on the insurance company as well as the type of life insurance coverage being purchased, some insurance companies may require a telephone interview as part of the application process.

Your one-stop online guide for life insurance quotes. Get free quotes now!

#2. Only Immediate Family Can Purchase It

Depending on which state you live in, the laws governing who is allowed to buy a life insurance policy for someone could come into play.

In general, you can bet that only immediate family or people related through marriage are able to purchase life insurance on another family member.

In most cases, people who have a financial interest in the survival of the person under the policy are also allowed to purchase coverage, but not own the actual life insurance policy.

If you have a low-income parent, buying a modest life insurance policy to cover funeral expenses and future medical bills is generally accepted.

Covering yourself in case of emergencies or debt demonstrates an “insurable interest” which insurance companies will look for when you buy life insurance for parents.

What is insurable interest?

To be an owner of another persons life insurance policy or be named as a beneficiary, there must be some type of financial connection between the insured and the individual that is owning the life insurance policy.

Insurable interest exists when the owner of the policy would encounter some type of a direct financial loss should the insured pass away.

Without there being an insurable interest, it will be highly unlikely that any insurance company will approve ownership of a life insurance policy on another individual’s life.

However, in the case that we are dealing with life insurance for parents, it is most likely an insurable interest present.

If you can foresee having a financial burden upon the death of your relative, buying a life insurance policy is a good idea.

#3. Deciding On The Amount

You need to do a little back of the envelope math to get an idea of what coverage amount your parent requires.

Think about how much income your parent has compared to the amount of debt or money owed on their mortgage. Give yourself at least $50,000-$100,000 to cover medical bills at the end of life. Then add another $10,000 for funeral expenses.

Consider purchasing or reserving burial plots beforehand. If you’re unsure, see whether your loved one would want a burial or a cremation.

It’s not unheard of to have a life insurance policy that covers the costs of paying off a mortgage.

Consider credit card debt and any loans that your loved one might have taken out. Taking out too high of an amount will raise a red flag for a policy provider, but too little could leave you with a financial burden.

When deciding on a total death benefit amount it is important that it shows financial justification to the insurance company.

What we mean by “financial justification” is that the death benefit amount cannot be any random number. Life insurance cannot be purchased with the intent to profit.

Insurance companies will look at the amount being applied and determine if there is enough financial justification to approve the amount being requested.

In order for the insurance company to determine whether or not the amount being applied for makes financial sense, they will often take into consideration:

- Annual income

- Unearned income

- Net-worth

- Other life insurance policies

One universal guideline used by most life insurance companies is the multiple times income method.

- Ages 20-40 can usually get up to 30x annual income

- Ages 41-50 can usually get up to 20x annual income

- Ages 51-60 can usually get up to 15x annual income

- Ages 61-69 can usually get up to 10x annual income

- Ages 70+ are qualified based on individual consideration

#4. Think About Policy Ownership

This section goes in part with what we mentioned earlier about insurable interest.

When underwriting notices that someone other than the insured is going to be the owner of a life insurance policy it can raise some questions.

If you’re buying life insurance for parents, there must be an insurable interest. Just because you’re their child is not reason enough to own their life insurance policy.

Their death must have some financial effect on you in order to be the owner of their life insurance policy.

It is also important to know that the person who owns the life insurance policy has the power to make changes and control the rights to the policy.

This means that not even the insured has any say so with regards to life insurance. In other words, the owner of the policy can make changes to the coverage amount, beneficiaries, billing payments, etc.

No information will be discussed with the insured with regards to the policy if the owner has not authorized so first. It is very important that the insured understands this if they are not going to be the owner of their own policy.

Your one-stop online guide for life insurance quotes. Get free quotes now!

#5. Figure Out Who’s Paying

The “payor” is just a term denoting who is signing the checks for insurance premiums.

The person who pays for the policy does not need to be the owner of the life insurance contract.

If you intend for your parents to own the policy but they cannot afford it, you as the child can pay for it without any problems.

So long as the premiums are paid on time, the policy will remain active. Policies differ but a lapse in payment could cause the policy to be voided.

#6. Determine The Beneficiary

Depending on the assets of the insured, the beneficiary might just be the next of kin, spouse, or child of the insured.

If there are large assets on the line, often people will leave some amount to their local church or a charitable organization they loved.

During the initial application process, there must be evidence of insurable interest when naming the beneficiary.

After the life insurance policy is active, the beneficiary could be any person, entity, or in some cases even a pet.

When buying life insurance for parents, ask who they want to benefit from any extra funds. Perhaps the proceeds should go to a charity or non-profit. Perhaps the parent would like to help grandchildren with college payments.

Be sure that the beneficiary or beneficiaries are clear to everyone involved.

#7. Decide On A Type of Life Insurance Coverage

Life insurance comes in all sorts of types from temporary to permanent. Although price can be an important deciding factor, be sure it doesn’t lead to it being a bad decision later in life.

Term Life Insurance for Elderly Parents

A term life insurance plan is fairly traditional and is based on a time frame, typically 10-30 years depending on the insured’s age when applying.

Term insurance is nice if you’re shopping based on price, but can become a costly later in life.

The problem with term insurance is that it’s very affordable, but it will eventually end as it’s only temporary life insurance.

Currently, age 80 is the oldest age to obtain a maximum term life insurance contract of 10 years. This means that after age 90, there are no options for life insurance coverage.

Permanent Life Insurance for Elderly Parents

Permanent life insurance is often thought of as the best life insurance coverage for senior or elderly parents.

There are two popular permanent life insurance options known as universal life insurance and whole life insurance. Both provide a lifetime of coverage with a fixed premium that is guaranteed to remain the same price throughout the entire contract.

Universal life insurance allows for larger death benefits at affordable prices. Applying requires full underwriting which can be difficult for parents with health problems.

Final expense plans are great options for older parents that require smaller amounts of life insurance protection.

These types of life insurance policies are designed for seniors that may not have the greatest health and are looking for an easy application process without the need for a medical exam.

Final Expense Life Insurance for Parents

- Whole Life Insurance

- Ideal for burial or final expense needs

- Usually comes in coverage amounts of $2,000 to $50,000

- No medical exam required

- Simplified application process

- Easier for parents with higher risk medical issues to qualify

Purchasing Life Insurance For Parents Can Be Easy

As long as you’re armed with the information you need to know in order to figure out which plan you want, you’ll find it’s not hard to get the insurance plan you need.

Knowledge is power and peace of mind is priceless. Get the best of both when you buy an insurance policy for your parents.

Interested in a life insurance policy for your parents? No problem. Top Quote Life Insurance is a great starting point. Our online website provides the ability to start instantly comparing life insurance rates from the highest-rated insurance companies in the United States.

Our licensed agents are also some of the best and are ready to help with any questions about insuring yourself or your parents.

We make applying for life insurance simple so please be sure to give us a call!

Ready to Compare Life Insurance Rates?

It’s free, fast and super simple.

Looking to compare life insurance prices? We can help. Enter your ZIP code to get free quotes from multiple insurers.

Your one-stop online guide for life insurance quotes. Get free quotes now!

Leslie Kasperowicz

Farmers CSR for 4 Years

Leslie Kasperowicz holds a BA in Social Sciences from the University of Winnipeg. She spent several years as a Farmers Insurance CSR, gaining a solid understanding of insurance products including home, life, auto, and commercial and working directly with insurance customers to understand their needs. She has since used that knowledge in her more than ten years as a writer, largely in the insur...

Farmers CSR for 4 Years

Editorial Guidelines: We are a free online resource for anyone interested in learning more about life insurance. Our goal is to be an objective, third-party resource for everything life insurance-related. We update our site regularly, and all content is reviewed by life insurance experts.