Full Review of the Best Guaranteed Universal Life Insurance

Free Life Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Leslie Kasperowicz

Farmers CSR for 4 Years

Leslie Kasperowicz holds a BA in Social Sciences from the University of Winnipeg. She spent several years as a Farmers Insurance CSR, gaining a solid understanding of insurance products including home, life, auto, and commercial and working directly with insurance customers to understand their needs. She has since used that knowledge in her more than ten years as a writer, largely in the insur...

Farmers CSR for 4 Years

UPDATED: Dec 4, 2023

It’s all about you. We want to help you make the right life insurance coverage choices.

Advertiser Disclosure: We strive to help you make confident life insurance decisions. Comparison shopping should be easy. We are not affiliated with any one life insurance provider and cannot guarantee quotes from any single provider.

Our insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different life insurance companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

Editorial Guidelines: We are a free online resource for anyone interested in learning more about life insurance. Our goal is to be an objective, third-party resource for everything life insurance-related. We update our site regularly, and all content is reviewed by life insurance experts.

UPDATED: Dec 4, 2023

It’s all about you. We want to help you make the right life insurance coverage choices.

Advertiser Disclosure: We strive to help you make confident life insurance decisions. Comparison shopping should be easy. We are not affiliated with any one life insurance provider and cannot guarantee quotes from any single provider.

Our insurance industry partnerships don’t influence our content. Our opinions are our own. To compare quotes from many different life insurance companies please enter your ZIP code on this page to use the free quote tool. The more quotes you compare, the more chances to save.

On This Page

Roughly 40% of Americans currently do not own any form of life insurance.

If you’re among them, you know you’re putting your family’s financial security at great risk. If something happens to you, will they be able to afford basic living expenses? Without your income, will they have to make sacrifices like selling the family home, taking on a second job, or facing tough decisions about your children’s future?

You need an affordable life insurance policy, but you also need permanent coverage.

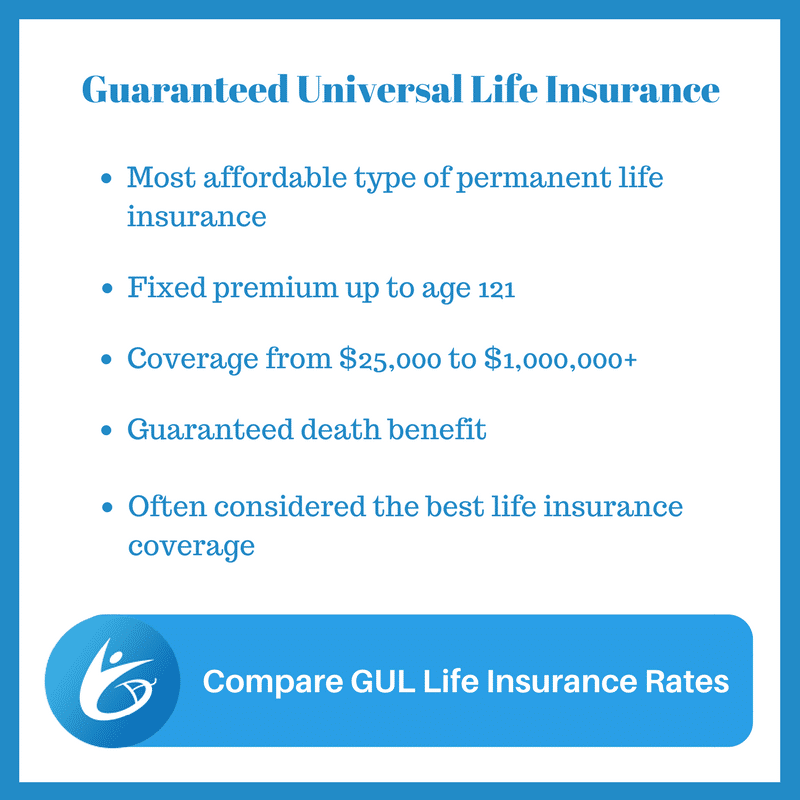

Guaranteed universal life insurance may be the solution you’ve been looking for, especially as it has the lowest premiums of any permanent life insurance policy.

Read on to learn more about what the coverage offers, who it’s best for, and the best providers currently offering guaranteed universal life insurance plans.

Looking to compare life insurance policies? We can help. Enter your ZIP code to get free quotes from multiple insurers.

What Is Guaranteed Universal Life Insurance?

Guaranteed universal life insurance is a type of permanent life insurance, that is designed to last your entire life.

It’s important to understand that, although similar in nature, guaranteed universal life insurance is not the same thing as whole life insurance. The two are often confused as being the same but are completely different.

Unlike term life insurance, guaranteed universal life insurance and whole life insurance policies do not expire (that is, as long as you continue to make your premium payments.) Permanent life insurance premiums will therefore be a bit higher when compared to payments associated with a term life insurance policy.

Both guaranteed universal and whole life insurance come with a cash value account that can grow over the life of the policy. You may be able to borrow tax-free from the cash value of either of these insurance plans.

Without spending too much time on the differences between guaranteed universal life and whole life insurance, the most significant factors that set these policies apart are the total cost of the policy, the flexibility that each can offer to the policyholder, and the overall amount of cash value growth that each is able to build.

Additionally, whole life insurance comes with a fixed premium payment, meaning that you’ll pay the same amount of money each time a payment is due. Fixed premium payments also apply to guaranteed universal life insurance policies.

However, guaranteed universal life insurance policies can offer flexibility with how and when premium payments are made. Whole life insurance does not.

But how is it that premium payments can be adjusted?

By the overall cash value of the account. In some cases, you might be able to use the cash value growth to completely skip payments if there is enough built up cash to cover to the premium payment.

Although guaranteed universal life insurance can offer this ability, be cautious in doing so, as it can lead to severe issues with the performance of the policy in future years.

Guaranteed universal life insurance policies are not designed to build much cash growth, so it is generally rare to even have enough cash growth to skip premium payments by utilizing the cash growth within the life insurance policy.

If you’re looking for a permanent life insurance policy with higher cash value growth potential, we suggest looking at an indexed universal life insurance policy.

You could also look into a whole life insurance policy that offers a guaranteed cash-value account, as well as the potential to earn dividends. However, they’ll be much more expensive than guaranteed life insurance.

In short?

Guaranteed universal life insurance focuses mainly on low-cost permanent coverage without significant cash build-up, whereas whole life insurance has the ability to build high cash values and is also permanent coverage, but it is much more expensive.

To summarize:

Guaranteed Universal Life Insurance Pros:

- Permanent coverage

- Guaranteed fixed premium

- Offers flexible payment lengths such as pay to age 85, 90, 95, 100, 110 & 121

- Most affordable permanent life insurance option

- Easy to structure the amount of coverage to your needs

- Volatile interest rates don’t impact premium payments

Guaranteed Universal Life Insurance Cons:

- Little to no cash growth

- More expensive than term life insurance

- Because of the lack of cash value growth, premiums need to be paid on time or it can have a negative effect on the future performance of the coverage fixed premium and duration of coverage

For additional information on the differences between guaranteed universal life insurance versus whole life insurance, as well as some of the other permanent life insurance coverage options, please check out our article titled “11 Best Types of Life Insurance Policies”.

Tip

Universal life insurance provides permanent fixed premium life insurance coverage that will never run out. It’s the most affordable form of permanent life insurance and your premium will never change from the time you purchase it to age 121.

Your one-stop online guide for life insurance quotes. Get free quotes now!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Permanent Life Insurance Backed with Guarantees

Who doesn’t like guarantees, especially when life insurance is involved?

Universal life insurance quotes offered through Top Quote Life Insurance are only from companies that provide guaranteed fixed premiums, as well as guaranteed coverage that will last to age 121.

Guaranteed life insurance is the best type of life insurance coverage if you’re looking for permanent life insurance coverage, but don’t want the expensive premiums associated with a whole life policy.

Our Review of the Best Guaranteed Universal Life Insurance Policies

Guaranteed universal life insurance has come a long way since its inception. Older universal life insurance policies did not have guarantees as they do now.

Unfortunately, many of the policies written prior to 2000 are under-performing and require additional premiums to keep them going. This causes a hardship for many people, especially for seniors.

In recent years, universal life insurance has made great changes. As a result, it has become a much more popular form of permanent life insurance coverage.

Since guaranteed universal life insurance is not offered through all life insurance companies, we at Top Quote Life Insurance have put together one of the best guides available to help you pick the best guaranteed universal life insurance policy.

TIP

Do you have an old under-performing universal life insurance policy that was purchased prior to 2000? If so, consider taking a look at any one of the below guaranteed universal life insurance companies.

If your old universal life insurance policy has some cash value you could do a 1035 exchange using the cash value towards a new guaranteed universal life insurance policy. This would reduce the overall cost for new coverage and provide new coverage that offers a guaranteed fixed premium and death benefit.

Be sure to reach out to us if you would like to discuss a 1035 exchange option using an old universal life insurance policy.

2020 Best Guaranteed Universal Life Insurance Companies

- AIG

- American National Life Insurance (ANICO)

- Banner Life Insurance Company

- Cincinnati Life Insurance Company

- John Hancock

- Lincoln Financial Group

- Mutual of Omaha

- Nationwide

- North American Company

- Pacific Life

- Principal Life

- Protective

- Prudential

- Sagicor

- Symetra

Quick Note on Some Common Policy Riders

Throughout our list of the best guaranteed universal life insurance companies, you will notice that every company will offer at least one or more policy riders. Depending on the company, some of the riders will be included free of cost with the life insurance coverage, while others will be available at an additional cost.

The following list is some of the more common policy riders that can be offered by most companies.

Accidental Death Benefit Rider: Pays out a second death benefit if death was the result of an accident.

Children’s Term Rider: Provides term life insurance coverage on the children of the insured, generally up to age 25. The coverage can often be converted to permanent coverage once the child has reached age 25 without having to provide evidence of insurability.

Terminal Illness Rider: Allows for the advancement of the death benefit should the insured become diagnosed with a qualifying terminal illness. This rider is generally available at no additional cost if offered by the life insurance company. This rider is also referred to as the accelerated death benefit rider as well.

Waiver of Premium: This rider waives all premium payments as a result of the insured becoming totally disabled and unable to work.

Your one-stop online guide for life insurance quotes. Get free quotes now!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

American General Life Insurance Company (AIG)

A.M. BEST’S RATING: (A) Excellent Rating

POLICY NAME: AG Secure Lifetime GUL III

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 121

HEALTH CLASSIFICATIONS: Preferred Plus, Preferred, Standard Plus, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $100,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 18-80)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accelerated Access Solution, Accidental Death Rider, Children’s Insurance Benefit Rider, Enhanced Surrender Value Rider, Lifestyle Income Solution, Spouse Rider, Terminal Illness Rider, Waiver of Premium Rider

ENHANCED SURRENDER VALUE OPTION – AG Secure Lifetime GUL III comes with a free built-in return of premium rider that allows for up to 100% of all premiums paid refunded back to the insured if coverage is no longer needed. This option is available in policy year 20 for a return of premium of 50% of all premiums paid. It is also available a second time in policy year 25 for a return of premium of 100% of all premiums paid up to 40% of the total death benefit.

ACCELERATED ACCESS SOLUTION – This is an optional policy rider available at an additional cost that provides tax-free income from the policy’s death benefit if diagnosed with a qualifying chronic illness. If qualified, a pre-determined portion of the death benefit will be paid every month.

LIFESTYLE INCOME SOLUTION – This is an optional policy rider available at an additional cost that provides access to the policy death benefit for income for any reason after age 85. Income is tax-free and the maximum amount that can be withdrawn is 10% per year.

TIP

The LifeStyle Income Solution Rider is a great option if you’re concerned about outliving your money in retirement years. This rider can provide a supplemental tax free income starting at age 85

QoL ACCELERATED BENEFIT RIDERS (ABR) – This rider comes free with AIG QoL Guarantee Plus GUL II which is a second guaranteed universal life insurance option offered by AIG. Other than a difference in price, the two coverage options are nearly identical and offer the same benefits and optional policy riders with the exception of the accelerated benefit riders. These riders are built into the coverage at no additional cost and can provide access to either a portion or even all of the death benefit due to a qualifying chronic, critical or terminal illness.

RELATED INFORMATION: Full AIG Life Insurance Company Review.

American National Life Insurance (ANICO)

![]()

A.M. BEST’S RATING: (A) Excellent Rating

POLICY NAME: Signature Guaranteed Universal Life Insurance

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 121

HEALTH CLASSIFICATIONS: Preferred Plus, Preferred, Standard Plus, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $25,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 18-80)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accelerated Benefit Riders (ABR), Children’s Term Insurance Rider, Disability Waiver of Premium Rider

GUARANTEED CASH OUT OPTION – Signature Guaranteed UL comes with a free return of premium rider that allows for a one time surrender within the first 60 days of the 15th, 20th, and 25th policy anniversary year. The return of premium amount is up to 65% of the premiums paid into the policy if surrendered at anniversary year 15 and up to 100% if surrendered at anniversary years 20 and 25.

ACCELERATED BENEFIT RIDERS – This is a free built-in policy rider that allows for early access to the policy death benefit due to a qualifying terminal illness critical illness or chronic illness.

NO MEDICAL EXAM UNDERWRITING – Coverage amounts under $250,000 can qualify for no medical exam underwriting as long as the applicant is under age 65. It is important to note that the best health classification will be at standard rates.

RELATED INFORMATION: Full ANICO Life Insurance Company Review.

Banner Life Insurance Company

A.M. BEST’S RATING: (A+) Superior Rating

POLICY NAME: Life Step UL

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 121

HEALTH CLASSIFICATIONS: Preferred Plus, Preferred, Standard Plus, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $50,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 20-85)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accelerated Death Benefit Rider (Terminal Illness Only)

FAMILY HISTORY: History of family cancer will not prevent consideration for preferred rates.

RELATED INFORMATION: Full Banner Life Insurance Company Review.

Your one-stop online guide for life insurance quotes. Get free quotes now!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Cincinnati Life Insurance Company

A.M. BEST’S RATING: (A+) Superior Rating

POLICY NAME: Lifesetter Flex UL

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 121

HEALTH CLASSIFICATIONS: Preferred Plus, Preferred, Standard Plus, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $50,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 18-75)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accelerated Benefit Rider (Included), Children’s Term Life Insurance Rider

ACCELERATED BENEFIT RIDER – This rider allows for access to the death benefit if diagnosed with a terminal illness which will result in death in less than two years. It also allows for early access if required to be confined to a nursing home for 90 days or longer.

TOBACCO CHEWERS – Non-smoking tobacco users such a chewers and cigar users can qualify for non-smoker rates.

RELATED INFORMATION: Full Cincinnati Life Insurance Company Review.

John Hancock

A.M. BEST’S RATING: (A+) Superior Rating

POLICY NAME: UL-G

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 121

HEALTH CLASSIFICATIONS: Preferred Plus, Preferred, Standard Plus, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $100,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 0-90)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accelerated Benefit (Terminal Illness), Disability Payment of Specified Premium, Long-Term Care

LONG-TERM CARE (LTC) Rider – This is an optional policy rider that is available at an additional cost that provides long term care protection. The rider works by paying out a pre-determined amount of funds from the policy death benefit to help pay for qualified long-term care expenses. The maximum monthly benefit will be based on either 1%, 2%, or 4% of the policy’s death benefit which is elected prior to coverage being issued.

QUIT SMOKING INCENTIVE: Provides current smokers with non-smoker rates for the first three policy years. If satisfactory evidence can be provided after year three that tobacco use has ceased, then non-tobacco rates will remain in effect. If tobacco use is evident then rates will be re-adjusted to reflect tobacco class.

RELATED INFORMATION: Full John Hancock Life Insurance Company Review.

Lincoln Financial Group

A.M. BEST’S RATING: (A+) Superior Rating

POLICY NAME: Life Guarantee UL

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 121

HEALTH CLASSIFICATIONS: Preferred Plus, Preferred, Standard Plus, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $100,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 20-85)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accelerated Benefit Rider with Critical Illness Coverage, Accidental Death Benefit Rider, Children’s Term Rider, Disability Waiver of Month Deduction Benefit, Disability Waiver of Specified Premium, Guaranteed Insurability Rider, Lincoln Life Enhance Rider, Minimum Death Benefit Endorsement, Spouse Term Rider

ACCELERATED BENEFIT RIDER WITH CRITICAL ILLNESS COVERAGE – This is a free rider that pays a portion of the death benefit in the event of a qualifying terminal illness, critical illness, or permanent confinement to a nursing home

- TERMINAL ILLNESS – The maximum amount that can be accelerated for a qualifying terminal illness is 50% of the death benefit, no greater than $250,000.

- CRITICAL ILLNESS – The maximum amount that can be accelerated for qualifying critical illness is 50% of the death benefit, no greater than $250,000.

- NURSING HOME – The maximum amount that can be accelerated for qualifying nursing home confinement is 40% of the death benefit, no greater than $250,000.

LINCOLN LIFE ENHANCE RIDER – This is an optional policy rider available at an additional cost that provides a portion of the policy’s death benefit if the insured is diagnosed with a qualifying chronic illness. The maximum amount that can be accelerated is up to 100% of the death benefit.

RELATED INFORMATION: Full Lincoln Financial Life Insurance Company Review.

Your one-stop online guide for life insurance quotes. Get free quotes now!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Mutual of Omaha Life Insurance Company

A.M. BEST’S RATING: (A+) Superior Rating

POLICY NAME: Guaranteed Universal Life

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 121

HEALTH CLASSIFICATIONS: Preferred Plus, Preferred, Standard Plus, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $50,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 18-85)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accelerated Death Benefit Riders, Accidental Death Benefit Rider, Association Group Disability Rider, Dependent Children’s Rider, Disability Waiver Rider, Guaranteed Insurability Rider, Guaranteed Refund Option, Waiver of Surrender Charges

ACCELERATED DEATH BENEFIT RIDER – This is a free rider that provides an advance payment of the policy’s death benefit in the event of a qualifying terminal illness or qualifying chronic illness.

- TERMINAL ILLNESS – The maximum amount that can be accelerated for a qualifying terminal illness is 80% of the death benefit, no greater than $1,000,000.

- CHRONIC ILLNESS – The maximum amount that can be accelerated for a qualifying chronic illness is 80% of the death benefit, no greater than $1,000,000.

GUARANTEED INSURABILITY RIDER – Provides the ability to add extra death benefit coverage without having to provide evidence of insurability.

GUARANTEED REFUND OPTION – Provides a guaranteed refund option if coverage is canceled in policy year 15 or policy years 20 through 25. Policy year 15 will be up to 50% of all premium paid refunded. Policy year 20, 21, 22, 23, 24, and 25 will be up to 100% of all premiums paid refunded.

NO MEDICAL EXAM UNDERWRITING – Option to purchase no medical exam coverage with coverage amounts from $50,000-$300,000 at standard health classification only. The maximum no medical exam amount for applicants ages 51-65 is $250,000.

RELATED INFORMATION: Full Mutual of Omaha Life Insurance Company Review.

Nationwide

A.M. BEST’S RATING: (A+) Superior Rating

POLICY NAME: No-Lapse Guaranteed UL II

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 120

HEALTH CLASSIFICATIONS: Preferred Plus, Preferred, Standard Plus, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $100,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 18-85)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accelerated Death Benefit Rider, Accidental Death Benefit Rider, Children’s Term Insurance Rider, Long-Term Care Rider II, Waiver of Monthly Deduction Rider

RETURN OF PREMIUM – Allows for a return of premium if coverage is canceled in policy year 16 or in policy year 21. If coverage is canceled in policy year 16, the refund amount will equal up to 50% of all premiums paid. If coverage is canceled in policy year 21, the refund will equal up to 100% of all premiums paid.

LONG-TERM CARE RIDER II – This is an optional policy rider that can be added to the life insurance coverage to help fund long term care expenses. The long term care rider allows for an acceleration of up to 100% policy’s death benefit.

RELATED INFORMATION: Full Nationwide Life Insurance Company Review.

North American Life Insurance Company

A.M. BEST’S RATING: (A+) Superior Rating

POLICY NAME: Custom Guarantee

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 121

HEALTH CLASSIFICATIONS: Preferred Plus, Preferred, Standard Plus, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $25,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 0-85)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accidental Death Benefit Rider, Accelerated Death Benefit, Children’s Term Rider, Guaranteed Insurability Rider, Waiver of Monthly Deduction Rider

ACCELERATED DEATH BENEFIT RIDER – This is a free rider that provides an advance payment of the policy’s death benefit in the event of a qualifying critical, chronic, or terminal illness.

- CRITICAL – Maximum amount of death benefit that may be accelerated for a qualifying critical illness is the lesser of 25% of the death benefit or a maximum of $50,000 per year.

- CHRONIC – Maximum amount of death benefit that may be accelerated for a qualifying chronic illness is the lesser of 24% of the death benefit or a maximum of $240,000 per year.

- TERMINAL – Maximum amount of death benefit that may be accelerated for a qualifying terminal illness is the lesser of 75% of the death benefit or a maximum of $750,000.

WRITEAWAY ACCELERATED UNDERWRITING – This program offers applicants who are between the ages of 18-60 and considered healthy an opportunity to skip the medical exam. The process is done utilizing an electronic application along with a telephone interview. Qualified applicants can be approved for coverage in as little as 72 hours.

RELATED INFORMATION: Full North American Life Insurance Company Review.

Your one-stop online guide for life insurance quotes. Get free quotes now!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Pacific Life

![]()

A.M. BEST’S RATING: (A+) Superior Rating

POLICY NAME: Pacific Prime UL-NLG

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 121

HEALTH CLASSIFICATIONS: Preferred Plus, Preferred, Standard Plus, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $50,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 20-80)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accelerated Living Benefit Rider (Terminal Only), Accidental Death Rider, Annual Renewable Term Rider (Additional Insured), Children’s Term Rider, Guaranteed Insurability Rider, Owner Waiver of Charges Rider, Premier Living Benefits Rider, Waiver of Charges Rider

ANNUAL RENEWABLE TERM RIDER – This rider provides an annual renewable term life insurance coverage protection to any member of the primary insured’s immediate family.

GUARANTEED INSURABILITY RIDER – Provides the option to increase the death benefit without any evidence of insurability. The option to increase the death benefit will be available at both specific policy anniversary dates or certain life events in which additional coverage may be needed such as marriage or birth of a child.

PREMIER LIVING BENEFITS RIDER – This rider provides an annual payment of the policy’s death benefit due to a chronic illness that is expected to be permanent. The maximum amount of death benefit that can be accelerated is 100% up to a lifetime maximum of $1.5 million.

RELATED INFORMATION: Full Pacific Life Insurance Company Review.

Principal Life

![]()

A.M. BEST’S RATING: (A+) Superior Rating

POLICY NAME: Universal Life Protector IV

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 121

HEALTH CLASSIFICATIONS: Preferred Plus, Preferred, Standard Plus, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $50,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 20-85)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accelerated Benefit Rider (Terminal Only), Children Term Insurance Rider, Cost of Living Increase Rider, Extended Coverage Rider, Salary Increase Rider, Waiver of Monthly Policy Charge Rider

COST OF LIVING INCREASE RIDER – This is a free rider that allows for an increase in the death benefit based on an increase in the Consumer Price Index (CPI). If an increase is accepted by the policy owner, it will result in an increase in premiums. However, if an increase is elected, it will not require evidence of insurability.

EXTENDED COVERAGE RIDER – This is a free rider that extends the maturity date of the life insurance policy to the insured’s date of death. For example, if the insured purchased the coverage to last to age 100 but lived past the maturity date, the rider would kick in to extend the coverage period ensuring that the death benefit will pay out past the maturity date of the policy.

SALARY INCREASE RIDER – This rider is only available for cases involving business life insurance coverage. When the rider is elected, it allows for additional life insurance to be purchased without evidence of insurability. In order for the rider to be used, the insured must be actively working and has received an increase in salary within the policy year that the rider is being requested.

RELATED INFORMATION: Full Principal Life Insurance Company Review.

Protective Life Insurance Company

A.M. BEST’S RATING: (A+) Superior Rating

POLICY NAME: Advantage Choice UL

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 121

HEALTH CLASSIFICATIONS: Preferred Plus, Preferred, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $100,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 18-85)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accidental Death Benefit Rider, Children’s Term Rider, Disability Benefit Rider, Extended Care Rider, Income Provider Option, Terminal Illness Rider

EXTEND CARE RIDER – This is a free rider that provides an advance payment of up to 100% of the policy’s death benefit in the event of a qualifying chronic illness.

DISABILITY BENEFIT RIDER – This is an optional policy rider that waives premium payments if the insured becomes totally disabled.

INCOME PROVIDER OPTION – Under most conditions, the death benefit is generally paid in full to the beneficiary. This option however allows the policy owner to structure how and when the death benefit funds are paid out to the beneficiary. Select a guaranteed monthly or annual income stream for the death benefit payout to the beneficiary for up to 30 years. This could be a very good option especially when the beneficiaries are minors.

RELATED INFORMATION: Full Protective Life Insurance Company Review.

Your one-stop online guide for life insurance quotes. Get free quotes now!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Prudential Life Insurance Company

A.M. BEST’S RATING: (A+) Superior Rating

POLICY NAME: PruLife Universal Protector

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 121

HEALTH CLASSIFICATIONS: Preferred Plus, Preferred, Standard Plus, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $50,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 0-85)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accidental Death Benefit, Children Level Term Rider, Enhanced Disability Benefit, Living Needs Benefit, Benefit Access Rider.

ENHANCED DISABILITY BENEFIT – This is an optional policy rider available at an additional cost that waives premiums if you become disabled.

LIVING NEEDS BENEFIT RIDER – This is a free rider that provides an advance payment of the policy’s death benefit in the event of a qualifying terminal illness or if required to permanently be confined to a nursing home.

BENEFIT ACCESS RIDER – This is an optional policy rider available at an additional cost that provides the insured the option to accelerate up to 100% of the policy’s death benefit should the insured become ill with a chronic or terminal illness. Applicants who choose this to purchase this rider will have the option to choose a monthly benefit amount of 2% or 4% based on their needs. Benefits received under this rider can be used for any purpose as there are restrictions on the funds received.

RELATED INFORMATION: Full Prudential Life Insurance Company Review.

Sagicor Life Insurance Company

A.M. BEST’S RATING: (A-) Excellent Rating

POLICY NAME: Sage No Lapse Universal Life Insurance

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 121

HEALTH CLASSIFICATIONS: Preferred, Standard Plus, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $25,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 0-85)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accelerated Benefit Insurance Rider, Accidental Death Benefit Rider, Children’s Term Rider, Waiver of Monthly Deductions Rider

ACCELERATED BENEFIT INSURANCE RIDER – This is a free rider that provides an advance payment of the policies death benefit in the event of a qualifying terminal illness or qualifying chronic illness.

- TERMINAL ILLNESS – The maximum amount that can be accelerated for a qualifying terminal illness is 25% of the death benefit, no greater than $400,000.

- CHRONIC ILLNESS – The maximum amount that can be accelerated for a qualifying chronic illness is 25% of the death benefit, no greater than $400,000.

ACCELEWRITING NO MEDICAL EXAM – Applicants who are between the ages of 16 to 65 and applying for coverage between $25,000 – $400,000 will not be required to take a medical exam.

RELATED INFORMATION: Full Sagicor Life Insurance Company Review.

Symetra

A.M. BEST’S RATING: (A) Excellent Rating

POLICY NAME: UL-G

TYPE OF POLICY: Guaranteed Universal Life Insurance

MAXIMUM COVERAGE LENGTH: Age 121

HEALTH CLASSIFICATIONS: Preferred Plus, Preferred, Standard Plus, Standard & Tobacco

MINIMUM COVERAGE AMOUNT: $100,000

MAXIMUM COVERAGE AMOUNT: $10,000,000+

ISSUE AGES: (Ages 16-85)

APPLICATION TYPE: Paper or Electronic

POLICY RIDERS: Accidental Death Benefit Rider, Additional Term Rider, Charitable Giving Benefit, Chronic Illness Plus Rider, Return of Premium (ROP)

CHRONIC ILLNESS RIDER – This is a free rider that provides an advance payment of the policies death benefit in the event of a qualifying terminal illness or qualifying chronic illness.

- TERMINAL ILLNESS – The maximum amount that can be accelerated for a qualifying terminal illness is 75% of the death benefit, no greater than $500,000.

- CHRONIC ILLNESS – The maximum amount that can be accelerated for a qualifying chronic illness is 50% of the death benefit, no greater than $500,000.

CHRONIC ILLNESS PLUS RIDER – This is an optional policy rider that that allows for up to 100% of the policy’s death benefit to be accessed in advanced due to a qualifying chronic illness. The monthly benefit is 2% and capped at the then current IRS per diem times 30.

CHARITABLE GIVING BENEFIT – This is an optional and free rider that allows the insured the option elect 1% of the policy death benefit up to $100,000 to go to a qualified charity of the policy owner’s choice.

RETURN OF PREMIUM RIDER – This rider allows for a 100% return of premium if coverage is canceled in either the 20th or 25th policy year. It should be noted that this rider is not free as it is with many other companies. However, the surrender window is 90 days, whereas other companies only give you 60 days to surrender.

Additional Term Rider – Adds a traditional 20 year term life insurance coverage to the guaranteed universal life insurance coverage.

Your one-stop online guide for life insurance quotes. Get free quotes now!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Guaranteed Universal Life Insurance Companies by Riders Offered

The below chart provides a quick break down of what riders and benefits are offered by each company. To reference back to any one of the companies listed, simply click on the company name in the left column.

| GUL Companies | Chronic Illness Rider | Critical Illness Rider | Long Term Care Rider | Nursing Home Benefit | Return of Premium | No Medical Exam Option |

|---|---|---|---|---|---|---|

| AIG | X | X | X | |||

| ANICO | X | X | X | X | ||

| Banner Life | ||||||

| Cincinnati Life | X | |||||

| John Hancock | X | |||||

| Lincoln Financial | X | X | X | |||

| Mutual of Omaha | X | X | X | |||

| Nationwide | X | X | ||||

| North American | X | X | X | |||

| Pacific Life | X | |||||

| Principal | ||||||

| Protective | X | |||||

| Prudential | X | X | ||||

| Sagicor | X | X | ||||

| Symetra | X | X |

NOTE: Some riders might not be available in certain states.

Guaranteed Universal Life Insurance Plans and Medical Exams

We know that, especially if your health is in decline, you may feel anxious about needing to take a medical exam in order to qualify for a life insurance policy.

First, the bad news: in most cases, you will most likely need to take a medical exam to be approved for a guaranteed universal life insurance policy. There are a few companies that do offer a no medical exam option as long as you meet the age requirement guidelines. These companies include ANICO, Mutual of Omaha, North American, and Sagicor.

However, the good news is that, once you’re approved for a guaranteed universal life insurance plan, you never have to take another medical exam again. This means that, even if your health begins to fail, or if your current health conditions take a sudden turn for the worse, the amount of your coverage will not be impacted in any way.

This, for many people, makes the slightly higher premiums than permanent life insurance plans require well worth it. When you apply for term life insurance, you’re at the mercy of the results of your medical exam when you need to renew or get a new policy.

What to Look for in a Guaranteed Universal Life Insurance Provider

All of the guaranteed universal life insurance companies and policies we’ve listed above are excellent options.

However, you need to find the policy that’s the best fit for your family, your financial situation, and your health.

So, what should you look for in a guaranteed universal life insurance provider?

First of all, take a look at the company ratings provided by agencies like A.M. Best and Standard and Poor’s ratings. If the company has a rating less than an A, it might be best to move on.

You may also want to ensure that you work with a provider that offers a “free look” period. This means that you can cancel your policy within the period, and still receive a complete refund. Also, speak with the provider about the fees associated with your plan — especially if you opt for one with an investment component.

Ask how much you’ll need to pay if, for any reason, you decide to cancel or surrender your policy before your death. However, remember that there is not much of a cash value buildup that the company could take surrender charges from. So, while it’s important to ask, you likely won’t need to worry about a surrender fee.

Your one-stop online guide for life insurance quotes. Get free quotes now!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Benefits of a Guaranteed Universal Life Insurance Policy

Now, let’s talk a bit more in detail about the benefits of a guaranteed universal life insurance policy.

Outside providing excellent permanent life insurance protection, many of these policies offer quite a few different policy riders such as living benefits, long term care benefits as well as return of premium options.

With proper planning, these benefits can be structured to really maximize the full potential of what a guaranteed universal life insurance policy can really offer outside of death benefit protection.

Chronic and Long Term Care Benefits

For example, longtermcare.gov reported that someone turning age 65 has a 70% chance of needing some type of long term care service in their remaining years.

The 2018 national median cost of long term care services ranged from $3,000 up to $8,000 per month depending on the level of services needed. Long term care costs are projected to rise every year.

One way to combat these potential costs is through the use of an affordable guaranteed universal life insurance plan that offers a chronic illness or long term care benefit rider.

A policy that offers these benefits can save you from having to spend your life savings, should the need for long term care services occur.

Critical Illness Benefits

Anyone who knows someone that has experienced a critical illness such as cancer, heart attack or stroke to name a few, understands the financial impact it could have on a family.

Having a life insurance policy with a critical illness rider can provide the funds to help cover what medical plans might not pick up. It can also provide funds to help pay for out of pockets expenses such as daily living expenses, childcare and household or medical bills not covered through health insurance.

Critical illness insurance is becoming a highly sought after insurance coverage option. Consider adding it to a guaranteed universal life insurance policy that can provide you with both critical illness and death benefit protection.

Return of Premium

It may seem a little odd having a return of premium option on a permanent life insurance policy, right?

However, this is actually an extremely great option to have available. For starters, it’s not uncommon for life insurance needs to change later in life. Having the option to surrender your coverage, if it is no longer needed, for up to 100% of every single premium paid can add up to a nice lump sum of cash.

That lump sum of cash can create a supplemental income for retirement, be reinvested into a single premium immediate annuity, or be used any other way you see fit. Best of all, the money received is tax-free.

Lastly, the return of premium option on a guaranteed universal life insurance plan can be utilized in many business planning strategies.

For example, this coverage can be purchased on a key person within the company. As with any key person life insurance policy, the death benefit is primarily used to help aid in replacing the key employee’s skills and protecting the business.

However, with a return of premium feature, it can come in handy should the key employee decide to leave the company. This allows the business owner to surrender the coverage for a full return of premiums paid.

This coverage can also come in handy when setting up a cross-purchase buy-sell arrangement. Should one partner pass away, the surviving partner may no longer need the life insurance coverage as the buy-sell agreement would not be needed. The return of premium option can allow for the surviving partner to cancel their coverage and receive a full refund of premium payments.

Tax Free Death Benefit

Remember that, under this plan, the death benefit given to your beneficiaries will be tax-free. Especially if you have a large estate, and if your beneficiaries stand to inherit more money than most people, this is an excellent way to ensure they can keep as much of it as possible.

As we mentioned earlier, you may even be able to transfer the cash surrender values from some of your other permanent life insurance policies to a guaranteed universal life insurance plan without having to pay taxes. This is done through a standard Section 1035 Exchange.

Instant Guaranteed Universal Life Insurance Quotes

Every company on our list of “The Best Guaranteed Universal Life Insurance” is offered through Top Quote Life Insurance. There are two simple ways to get guaranteed universal life insurance quotes with Top Quote Life Insurance.

A licensed Top Quote Life Insurance agent will be able to answer any questions you might have pertaining to any one of the guaranteed universal life insurance companies reviewed in this article. They will also be able to provide you with quotes for coverage, as well as any optional riders that you might be interested in.

A second and most convenient way is through our online quoter which can be located at the top right of this page or if you’re on a desktop to the right of your screen. Both of these options will allow you to instantly view sample rates right from your desktop, tablet or mobile device.

When viewing rates for guaranteed universal life insurance be sure to select “lifetime” as the type of insurance. This will quote only the companies that offer a guaranteed universal life insurance option.

We hope you enjoyed our review of the Best Guaranteed Universal Life Insurance Companies and as always please be sure to reach out to us for assistance.

Ready to Compare Life Insurance Rates?

It’s free, fast and super simple.

Looking to compare life insurance policies? We can help. Enter your ZIP code to get free quotes from multiple insurers.

Your one-stop online guide for life insurance quotes. Get free quotes now!

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Leslie Kasperowicz

Farmers CSR for 4 Years

Leslie Kasperowicz holds a BA in Social Sciences from the University of Winnipeg. She spent several years as a Farmers Insurance CSR, gaining a solid understanding of insurance products including home, life, auto, and commercial and working directly with insurance customers to understand their needs. She has since used that knowledge in her more than ten years as a writer, largely in the insur...

Farmers CSR for 4 Years

Editorial Guidelines: We are a free online resource for anyone interested in learning more about life insurance. Our goal is to be an objective, third-party resource for everything life insurance-related. We update our site regularly, and all content is reviewed by life insurance experts.